The importance of diversification for revenue growth

In June 2024, TV manufacturers were desperately seeking price concessions from panel makers because their profit margins were decreasing. This is largely the combination of panel price hikes and a surge in shipping prices in recent months but heightened by growing concerns about slowing consumer demand and intensifying marketing competition. TV manufacturers are now vying for market share with lower prices, or they risk rising inventory or to opt for downsizing their shipment targets. Shipping costs also surged in the earlier part of 2024, and the impacts on larger sized LCD TVs are significant compared with the low base in late 2023.

Entering the middle of the year, several top-tier TV brands cut their 2024 TV business plans by 4–5% compared with their early forecasts. China’s top-tier TV brands have been the main source of demand growth in the past years, but they are now facing more challenges not only in China but also in the US market. Chinese TV brands are already disappointed by weak TV sales during China’s 618 shopping festival and are facing growing competition in the US market, where TV prices are distorted.

In response to weakening demand, major panel makers plan to lower their flat panel display (fab) utilization to stabilize panel prices. On the other hand, some are giving special support to selective and strategic TV customers to drive traffic in the market. TV manufacturers are becoming more concerned about the possibility of panel makers drastically changing their fab utilization when panel prices are at risk of declining. There are also concerns about the increasing risk of overbuilding inventories and deteriorating profit margins. Additionally, the scenarios of LG Display selling its LCD fab in China and Sharp announcing a halt to its LCD TV panel production in Japan in September 2024 remain a concern. TV manufacturers continue to face challenges with profitability within their core manufacturing business.

In recent times we’ve seen the adoption of free-ad supported streaming TV (FAST) channels, new TV advertising models, and more recently shoppable TV advertising.

While the FAST market trajectories will diverge internationally, it is important to understand how they are evolving and how they intertwine with diversification of revenue streams.

The US FAST market has followed the pay-TV market blueprint, with CTV platforms emerging as key gatekeepers in this space. European broadcasters are, by contrast, better positioned to retain control over the linear viewing experience, which can negate the need for FAST channels.

Omdia previously observed that the US FAST market was on a trajectory to become pay TV 2.0, with CTV platforms following the pay-TV playbook when it comes to channel carriage and ad inventory sharing models. In 2024, this trend will come full circle. The Comcast and Charter joint venture, Xumo, as well as the slate of devices powered by this platform, will begin to transform pay-TV operators into CTV platforms. Major channel groups will make strides toward FAST distribution. Paramount’s Pluto TV, an early FAST pioneer, will accelerate the pivot upstream, having positioned itself as a channel package licenser supplying CTV platforms. Indeed, through platforms like Samsung TV Plus, LG Channels, and Vizio WatchFree+, CTV manufacturers themselves are now crucial gatekeepers – and service operators – in the FAST space.

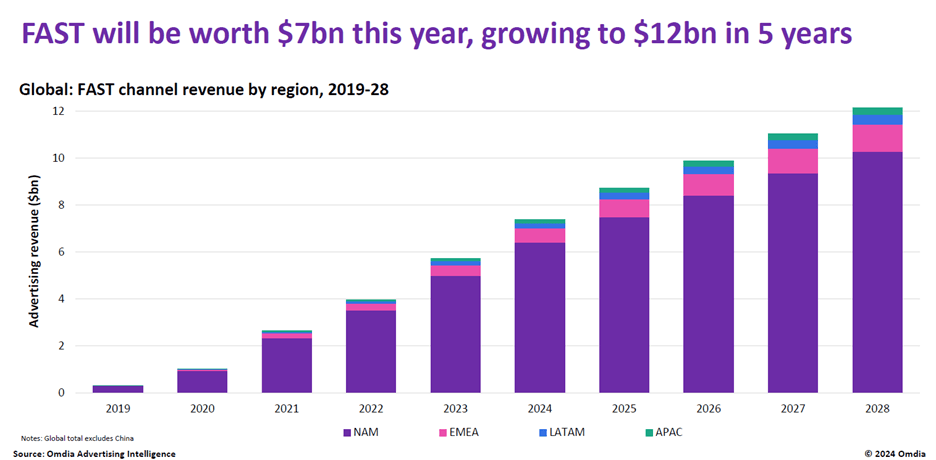

While global FAST revenue is dominated in the North American market, there is significant growth projected over the next five years in other regions, with expanding European, Latin America and Asia-Pacific scope.

The opportunity is evolving as fast as the technology is innovating, and manufacturers must analyze all avenues and identify if they want to partner with or become content owners, identify the technology to invest or acquire, as well as understanding the ad tech ecosystem. Now is the time to understand where they fit to seize the new opportunities.