The battle for attention is provoking industry consolidation and new kinds of strategic partnerships

The move away from traditional media, towards digital, is intensifying and is bringing with it a series of moves towards consolidation. This is based on the, logical, perception that market consolidation gives local players the scale they need to push back against global streaming growth.

In mid-2025 RTL Group moved to acquire 100% of Sky Deutschland from owner Comcast to create a group with a total of 11.5 million subscribers in Germany, Austria, and Switzerland, operating in free TV, pay TV, and, of course, online. The transaction is expected to close in 2026, subject to regulatory approvals. RTL will pay €150m ($176m) in cash, as well as an additional payment of up to €377m based on share price performance over the next five years. The company stated the reasoning behind the deal was that “together, the business is well positioned to meet evolving consumer demands and compete with global streamers.”

This deal followed the signing of a new distribution agreement between Netflix and local French broadcaster TF1, which will formally launch in France in the summer of 2026. The partnership will see Netflix host TF1’s linear and on-demand content entirely within the Netflix interface.

Although Netflix has sealed numerous distribution partnerships with local players over the last decade, this deal breaks new ground by effectively positioning Netflix as an aggregator, with all five TF1 linear channels as well as on-demand content from its TF1+ platform available within Netflix packages in France. It represents another step in the company’s evolution as it continues to compete with long-established players in the media and entertainment industry. Almost all of Netflix’s decisions and developments that it has implemented in the last few years—whether that be its ad-supported tier, its account sharing crackdown, or its push into live events—have stemmed from a shift in focus from subscriptions to revenue – and the need for increasing engagement to drive it – as its primary measure of growth.

Competition for eyeballs is taking place not only within the TV and streaming space, but across all online tech and media consumption. And, while this deal should enable TF1 to recapture the linear TV audiences that have been lost to Netflix and other global streamers in recent years, it does risk cannibalization of the broadcaster’s current growth engine, TF1+, which Omdia is forecasting to account for over a fifth of TF1’s ad revenue by 2030.

With Netflix ad loads being typically lower than those on BVOD services like TF1+, and uncertainty regarding the flow of viewing data between the two companies, this certainly represents something of a risk for the French broadcaster. However, the deal also represents an opportunity for TF1 to expand its reach to lapsed TV viewers who are not current users of its TF1+ service and, within this context, could still offer a complementary revenue stream to its owned-and-operated (O&O) streaming business.

Rodolphe Belmer, chief executive of TF1, commented on AFP that the deal would “enable our content to reach unparalleled audiences and unlock new reach for advertisers,” adding that TF1 expected it to “bring a net benefit in audience reach.”

The partnership will also give Netflix a serendipitous route to more live sports content, which Netflix has been cautiously pursuing with a handful of special events and established regular seasonal matches. Sports rights remain expensive (TF1 opted not to bid for rights to the next year’s FIFA World Cup) but the partnership could enable the broadcaster to invest more, given the claimed revenue upside. TF1 currently has a wide-ranging rights agreement for the French men’s national team qualification matches in UEFA and FIFA competitions through to 2028.

Both the RTL and TFI deals are examples of European groups honing their strategy in a market where consumers are increasingly doing more of their video consumption online. While RTL Group is bullish about the prospects of growth in subscriptions, beyond that metric the deal will also give it an important boost in the all-important battle for customer attention.

Gaining and retaining engagement is now key to monetization and, for companies like RTL, the benefits that consolidating with other local players will bring are clear in an increasingly competitive market. RTL has been working in partnership with Sky for the last two years, sub-licensing rights to key sports events, including Formula One motor racing and Bundesliga football. On an investor call with the company, CEO Thomas Rabe described the two groups as “highly complementary,” given RTL’s main focus on advertiser-funded channels and Sky’s subscription revenue. Rabe also highlighted the operational continuity of the deal, noting that Sky would continue to use Comcast’s technology platform, as well as acquiring movie and TV content from NBC Universal.

Sky Deutschland’s extensive portfolio of premium sports rights is one of the key reasons RTL is pursuing its acquisition. These rights, which include the Bundesliga (secured until 2029), DFB-Pokal, Formula One, and the Premier League, are critical assets in a market where live sports remain one of the few reliable drivers of large-scale TV audiences and subscriber engagement. Sports content not only delivers “appointment viewing”—a crucial factor for ad sales and audience retention—but also provides opportunities for cross-promotion, bundling, and long-term value creation.

For RTL, these assets align seamlessly with its existing rights portfolio, which includes highlight rights for the Bundesliga on RTL+ and free-to-air rights for the second division’s top weekly match. RTL is also home to UEFA Europa League and UEFA Europa Conference League matches, further solidifying its position as a key player in sports broadcasting. By combining these rights with Sky’s offerings, RTL can create a comprehensive sports ecosystem that appeals to both linear TV and streaming audiences, while also avoiding costly bidding wars for Bundesliga rights in the near future.

The acquisition also represents a significant opportunity for RTL to accelerate its streaming ambitions. RTL+ has carved out a niche with a younger, more female audience, while Sky’s streaming service, WOW, attracts a predominantly male, sports-focused demographic. Together, the two platforms offer a complementary audience base that could help RTL achieve the critical mass needed to compete with global streaming giants such as Netflix and Amazon Prime Video. By bundling Sky/WOW with RTL+ and leveraging its free-to-air channels to promote Bundesliga matches, RTL can create a compelling value proposition for consumers.

While the Sky deal will allow RTL to become the third leading online subscription player at a stroke (moving ahead of Disney+ and behind Netflix and Amazon), next year will see the launch of HBO Max and the end of the output and production deal between the US company and Sky, which has included the rights to high-end TV series such as House of the Dragon, The White Lotus, and The Last of Us. A bundling agreement between Sky and WB Discovery has already been negotiated in the UK and would seem the best option in the German-speaking territories. However, when asked if the merged company would look to emulate the TF1 distribution deal in France, Rabe declined to dismiss the possibility, so raising the possibility of additional deals on the horizon.

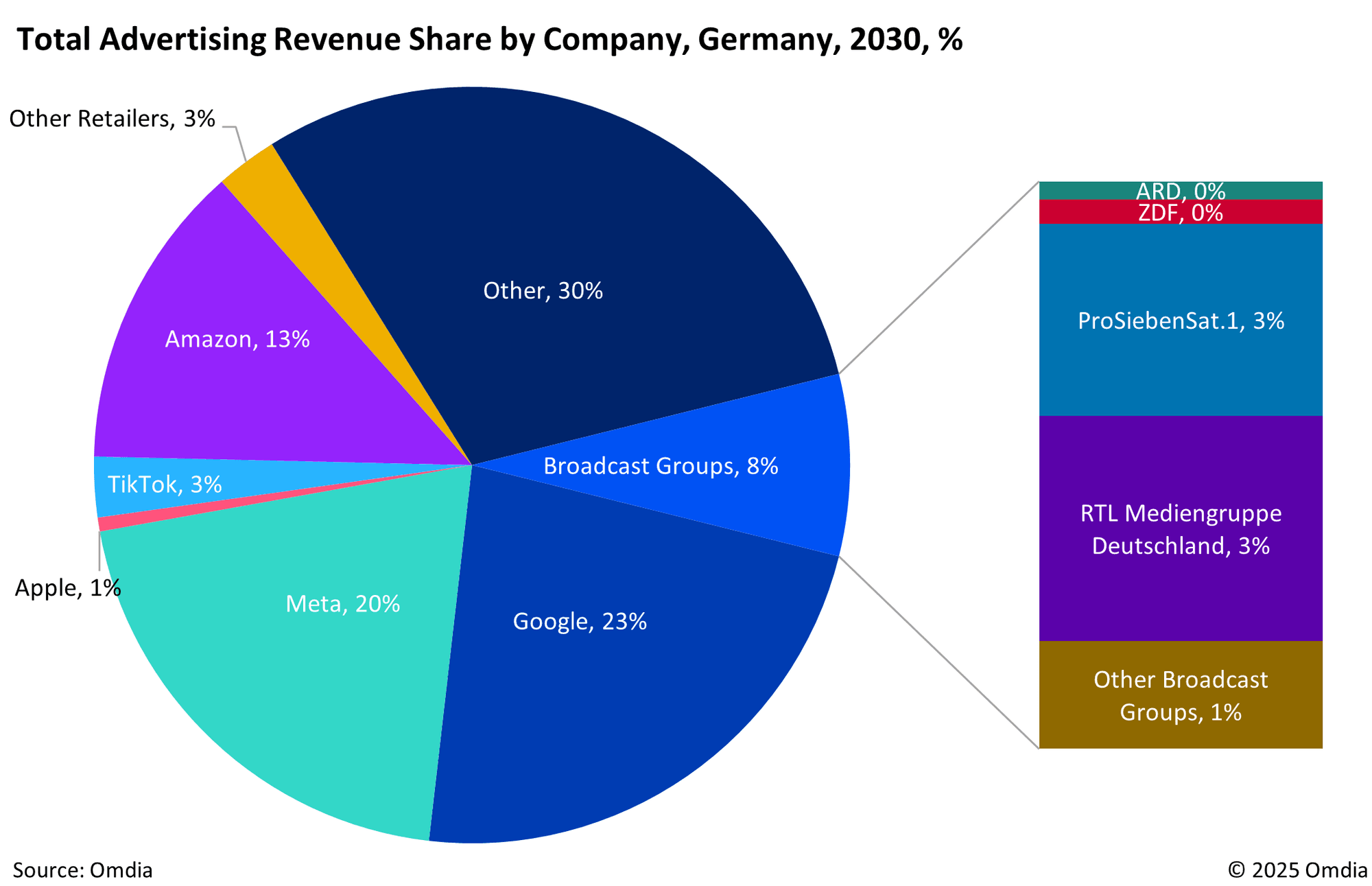

Several previous attempts at mergers have been attempted by major media companies as they seek to build the scale and resources needed to compete with the big techs. In most cases, the plans have been foiled by regulatory intervention over competition concerns. However, that reasoning defies the logic of current reality: in 2024, Google, Amazon, Meta, and Apple collectively took almost half of ad revenue in Western Europe and, by 2030, this will have risen to 56%. By way of contrast, a combined RTL Deutschland and Sky Deutschland will take less than 5% of ad revenue generated in Germany over the next five years. However, both players hope the synergies and scale created by any combination will reverse this trend, especially as more viewing shifts to online platforms.

Omdia expects competition authorities to soften their stance on broadcaster consolidation as the reality of big tech’s ad dominance starts to sink in. Germany is as yet unproven ground for this, but the deal between RTL and Sky Deutschland is likely to go ahead as planned. This, in turn, could mark a watershed moment in European broadcasters’ attempts to stave off the threat of digital giants through consolidation. Whether this will be as effective as partnering with those digital giants, however, remains to be seen.