Ad tech: the critical link between engagement and monetization

The growing prioritization of engagement among broadcasters and streamers is largely reflective of a shift from subscription-focused monetization strategies to ad-supported business models. Most major streamers now offer ad-supported versions of their services internationally, and this trend is set to continue for the foreseeable future. Meanwhile, the need for broadcasters shift linear TV spend to their owned-and-operated BVOD platforms, rather than the growing competition across the CTV space, will only intensify in the coming years. All this means that the volume of video ad inventory addressable to ad tech vendors is increasing significantly.

But adding effective advertising into the streaming video mix is not a simple process. The ad tech value and supply chains are complex, and video advertising in particular increases this complexity – especially for players operating across live and linear (i.e. FAST) environments, in addition to ad-supported video on demand (AVOD). Technologies such as server-side ad insertion (SSAI) take on a much more pronounced role in this environment, for instance, in addition to broader programmatic ad technologies. Meanwhile, the need to ensure interoperability with a shifting TV measurement landscape creates further challenges – or opportunities for some vendors.

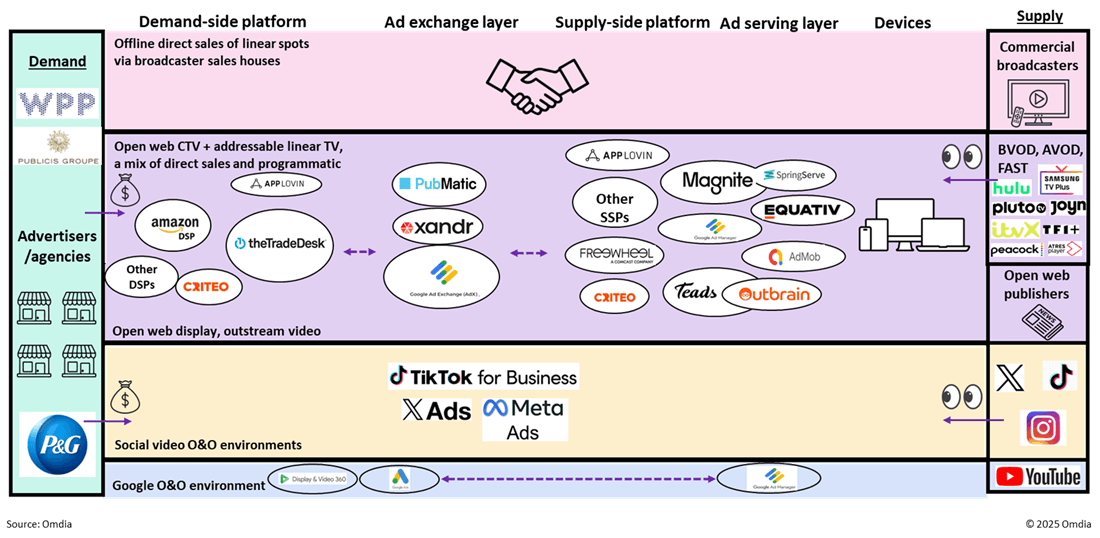

The video ad tech space also has very different competitive dynamics than that seen across the broader display ad market, which is largely dominated by just two players: Google and Meta. In the open programmatic display space, Google is by far the most dominant force on a global scale.

However, the preeminence enjoyed by Google in display ad tech is not replicated in video: the publisher landscape is more consolidated than in display, TV device OEMs/OSs are actively encroaching on the flow of ad dollars, programmatic execution is in its infancy, and certain players (e.g., Netflix) are building out their own ad stacks. Where linear TV consumption has remained relatively resilient, such as in Continental Europe, ad trading will likely remain significantly offline and not addressable to the programmatic ecosystem for some time. Where it will come online, publishers, particularly larger broadcasters, will prefer to sell inventory directly to advertisers but with the use of programmatic and automated mechanisms, otherwise known as “programmatic guaranteed.” Because of the lower number of intermediaries involved in such deals than in the world of open programmatic, ad tech revenue on offer for the likes of Google is diminished.

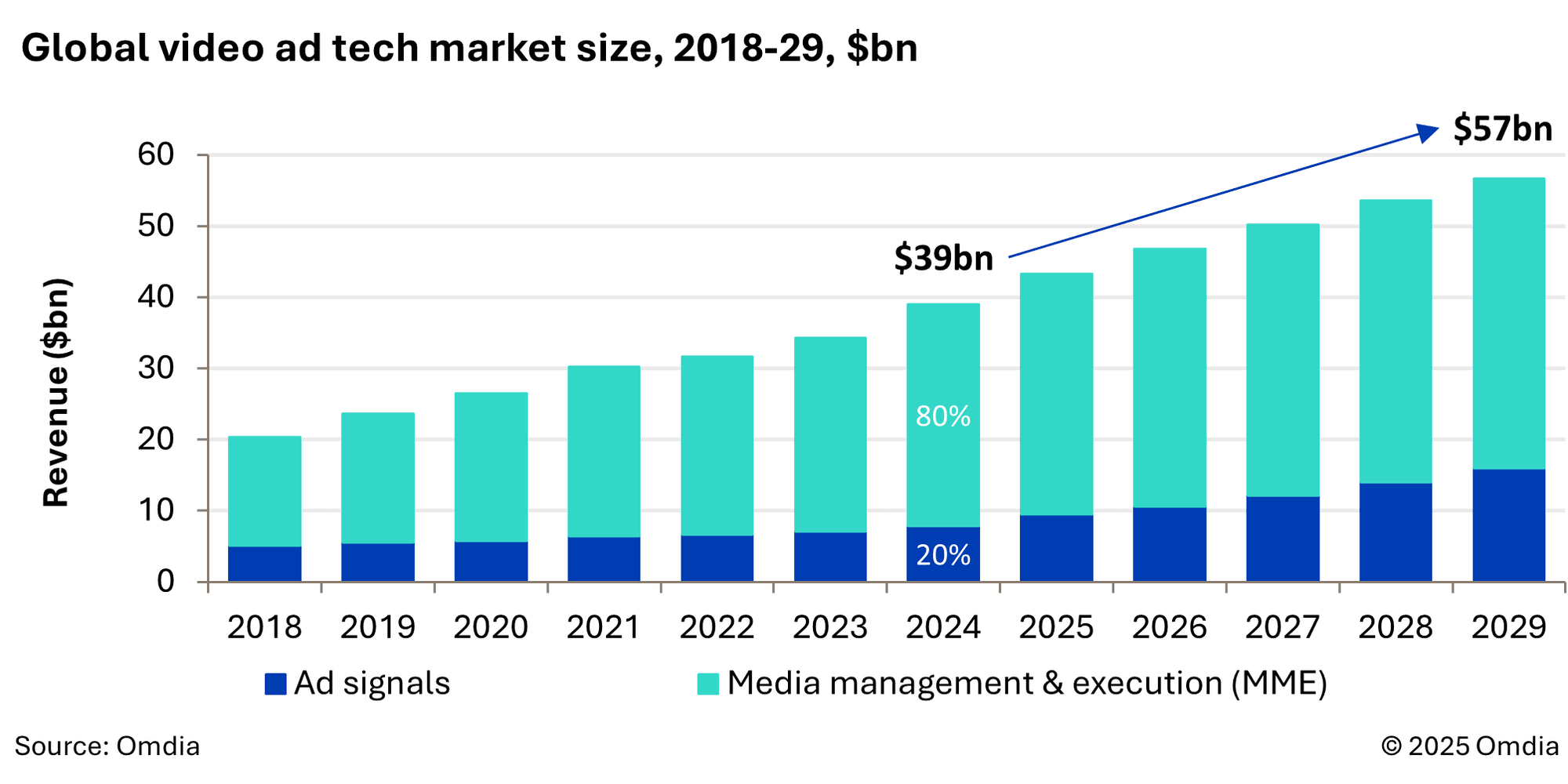

Though Google enjoys a leading position in the media management and execution (MME) segment – which accounts for around 80% of total video ad tech market revenue – this has been subject to encroachment by other vendors. In 2024 it accounted for a 15% share of the market by revenue, down from 18% in 2023. Big gainers include The Trade Desk, Amazon, AppLovin, and Comcast’s Freewheel. For reference, MME is an aggregated category of vendors involved in ad insertion, management, serving, and trading; DSPs; and SSPs.

Notably, MME’s share of the overall video ad tech market is set to fall from 80% in 2024 to 72% in 2030. This will come as the ad signal segment (composed of ad trading, effectiveness, quality, addressability, viewability measurement, and contextual advertising) grows at a faster rate as ad inventory differentiation, first-party data, cross-platform audience tracking, and ad environment quality become progressively more important to publishers and advertisers. In all, video ad tech revenues will grow at a 7.7% CAGR between 2024 and 2029 to reach a value of $57bn.

Video has been a significant growth area for The Trade Desk, which is looking to leverage its strength as a DSP to offer OEMs and publishers an attractive deal on ad economics at the frontend through its upcoming new TV OS, Ventura. Amazon has maintained exclusive domain over its growing CTV inventory pool via its own DSP, which now includes that of Disney+ and Roku Channel, and will improve its platform control and monetization as it reportedly aims to build out its own OS, Vega, into its device footprint. Though Google will remain a leading presence as the programmatic TV ecosystem grows and more video ad inventory comes online, its ability to influence outcomes is more limited than in display, mobile, and search.

Concerns remain over the full implementation of programmatic ad tech within TV and CTV from the sell side due to a perceived danger of replicating the commoditization of ad inventory that publishers have experienced in online display. Of course, commercial broadcasters recognize the benefits of creating ad tech platforms of their own to optimize ad execution and provide a broader universe of targetable segments for the buy side than in linear; however, this will be done on their own terms. ITV’s Planet V addressable ad platform is a good example, where a third party builds out the necessary infrastructure, but ITV remains the controlling party (with other broadcasters running their inventory through it). It is a similar story in measurement: the CFlight initiative in the UK to implement cross-media measurement is a case in point.

The impulse to cooperate among broadcasters is stronger than the impulse to dive headlong into open web programmatic. The pooling of premium differentiated ad inventory is a source of strength. A similar impulse is of course true for Tier 1 SVOD/AVOD hybrids as they scale up their proprietary ad infrastructure to give them fullest possible control of their inventory. Ad tech players that remain content agnostic while also bringing scaled demand will have the best opportunity to fully access this emerging CTV ecosystem. All things considered, broadcasters and OTT video players should continue to focus on developing their own in-house ad tech, or at least strengthen exclusive partnerships with key video-and-CTV-focused ad tech vendors.