Turning engagement into sales: the rapid convergence of TV and retail media

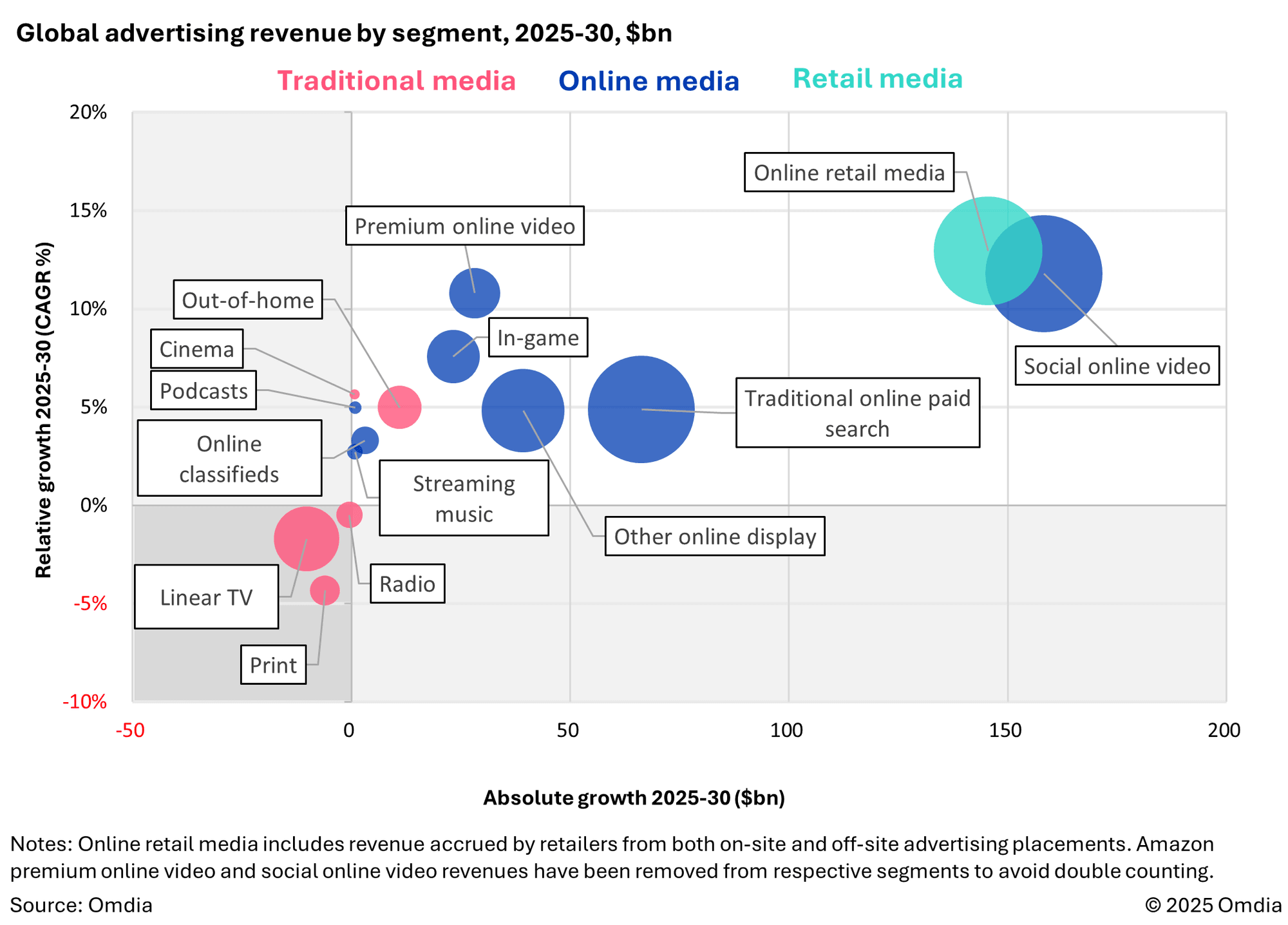

Retail media, which sees retailers place ads across their own and partners’ online properties, has quickly emerged as one of the fastest-growing segments of the global advertising market. Globally, retailers effectively doubled their online advertising revenue from 2020 to 2024, reaching $144bn amid a global e-commerce boom – overtaking the entire linear TV ad segment in the process. This will grow to almost $300bn by 2030 as retail media becomes a core aspect of retailers’ profitability strategies and continues to augment the connection between buyers and sellers, closing the loop on online sales attribution in the process.

Retail media’s rise coincides with an accelerating shift from traditional to digital media, which is forcing some of the biggest incumbent media players to become more focused on delivering outcomes rather than just impressions. Folding commerce and retail data into the mix—particularly when it comes to connected TV (CTV)—will be a game-changer in pushing up the value and reach of retail media, especially in mature markets where linear TV consumption is declining rapidly.

But, while retailers themselves currently drive most of the revenues being generated in this growth segment through onsite placements, the shift towards offsite retail media – which sees ads being targeted and tracked using retail data on third-party sites and apps – is expanding the opportunity to other players across the technology, media, and telecoms (TMT) value chain. By 2030, Omdia estimates that over $85bn in annual revenue will be generated by non-retailers (e.g., media firms, ad tech vendors, and other intermediaries) from retail media operations. This represents an expansion of over 4× compared to the equivalent revenue generated in 2024. Yet challenges remain around the role of data, measurement, and business models before this value can be unlocked fully.

Onsite search remains the largest individual retail media segment, buoyed by its proximity to the point of purchase and intent to buy. Yet, display’s share will grow over the forecast period as growth in search activity—and inventory—starts to slow on retailers’ sites and apps. This will come as retailers look to fill more blank space on their sites and apps with monetizable display ad units, including video.

However, there will be a limit to the number of display ads on retailer sites and apps before they become a hindrance to their core functionality of delivering enjoyable, frictionless shopping experiences. There will also be a limit to the number of advertisers for onsite placements, mostly limited to retailers’ pre-existing partner brands.

To capture more advertisers and alleviate inventory saturation, retail media needs to move up the marketing funnel to other areas of media. Some of the biggest retailers are doing this with their own ad-funded media properties, but most retailers are instead pivoting to offsite display, which sees retail data used to target and track ads across third-party media, usually on a programmatic basis. Offsite display is already the biggest revenue driver for many retail media networks.

Although offsite display will be the fastest-growing segment between 2025 and 2030, expanding at a CAGR of 27%, it will still only account for 11% of net ad revenue—or $36bn—accrued by retailers by the end of the forecast period.

However, the offsite display segment offers substantial revenue opportunities for other stakeholders, not just retailers, including media companies and ad tech intermediaries. Indeed, when adding their offsite display revenue on top of that of retailers—thereby producing a gross, rather than net, figure—the offsite display segment is projected to reach $119bn in 2030, exceeding onsite display ad revenue.

As such, offsite retail media will be an increasingly important segment for many media owners over the forecast period, particularly those in the CTV segment. It also represents an opportunity for the biggest retailers to challenge ad tech incumbents by scaling up their own ad tech businesses. Disney and Amazon, for instance, entered a deal in June 2025 that will see Disney’s OTT ad inventory become available on Amazon DSP. A similar deal was also announced between Roku and Amazon in the same week. Indeed, retail media networks could well become the new standard given the increasing shift of various media to delivering outcomes, and the ongoing death of third-party cookies.

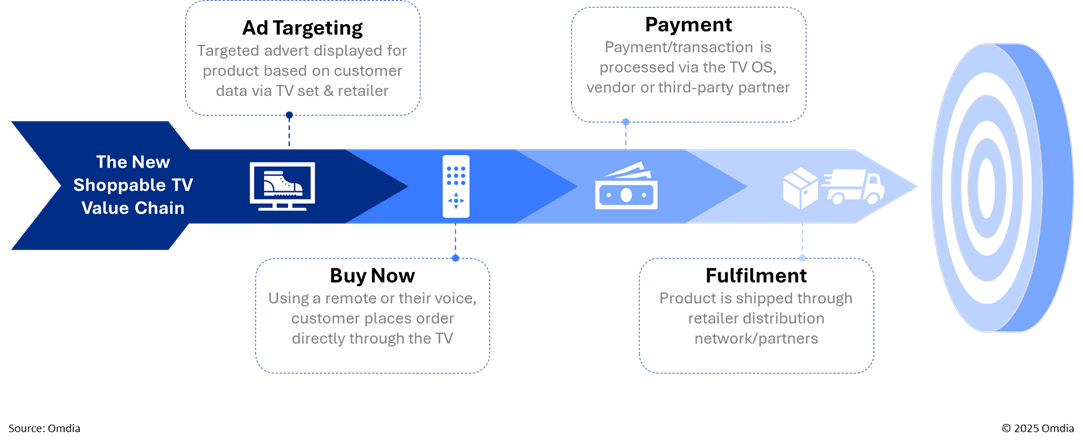

The most direct means of tying ad spend to actual purchases is, naturally, shoppable media. As TV and video incumbents move further down the marketing funnel, Omdia expects much more focus to be paid to directly shoppable TV advertising – an area already being explored by multiple major incumbent players.

This comes as TV incumbents are facing the need to deliver outcomes for advertisers and much stiffer competition in CTV than they have in traditional linear TV. Decades-long rivalries between broadcasters and channel groups continue in the CTV market, but it also marks the introduction of OTT new entrants, such as Netflix and YouTube, and CTV manufacturers and platform operators into the mix. And, crucially, some of these are also retailers—most notably, Amazon and the ad-supported tier of its already popular Prime Video service, which, globally, reaches 200 million ad-supported users per month and will drive CTV’s share of Amazon’s onsite ad revenue to 30% by 2030.

In May 2024, Amazon introduced shoppable ad units on Prime Video in the US and will expand their availability to the UK in 2H25. Amazon is not the first to bring shoppable video ads to CTV, but it is uniquely positioned to fulfil the whole process—from AI-powered ad creative and programmatic targeting to media consumption, payment facilitation, and even product delivery. Advertisers have largely taken an experimental approach thus far, but Omdia expects many advertisers—and other CTV players—to grow investment in shoppable TV to 2030.

Yet, outside of Amazon’s walled garden, there remains multiple points of friction in the shoppable TV value chain that must be overcome before it becomes a tangible revenue stream.

For instance, effectively positioning shoppable TV ads will require greater standardization of first-and-third-party data flows, in addition to the development of contextual targeting options. Frictionless on-device (and in-stream) purchasing methods will require integration at the hardware and UI level on CTV devices, as well as robust payment security technologies. And, most importantly, the mass-market logistics of shoppable TV – i.e. local stock levels and fulfillment – will need account for a highly fragmented retail landscape, especially in diverse regions like Europe.

Even so, the upside is clear for those that can crack the shoppable TV opportunity – while the entire media and entertainment industry will be worth $1.3tn in 2029, online spend by consumers will reach $6.6tn in the same year.